| Type of paper: | Report |

| Categories: | Banking |

| Pages: | 6 |

| Wordcount: | 1582 words |

Overview HSBC Middle East

HSBC Bank has the largest representation in the Middle East of any international financial institution. HSBC Bank Middle East runs a vast network of branches providing banking products in over ten countries including Algeria, Bahrain, Israel, Kuwait, Qatar, Egypt, Lebanon, Oman and United Arab Emirates (UAE). The wide network of twenty-four branches in UAE makes the country essential to its regional business. Although ceased operating in Djibouti, and Jordan, HSBC adopts a market-led pursuit of opportunities to offer profitable financing-focused solutions to Middle East corporations and residents. HSBC Middle East capitalizes banking services arranged in London yet delivered through integrated basis to match local requirements. HSBC offers Islamic banking targeting the dominant audience alongside the investment, transaction, and global advisory finance services. However, the bank has continually evolved to adapt to changing market requirements without losing its international brand identity. HSBC wide geographic presence in the Middle East region demonstrates a historic partnership and progress applicable to other companies seeking the regional success.

Changing financial requirements in Middle East region to embrace the global trend and mushrooming of business hubs yields profitable opportunities for HSBC to serve the international and regional clientele. Such reflects in shifting its head office from Jersey to Dubai Financial Centre to ensure proximal location near the regional clientele it serves. HSBC foothold in the Middle East region yields unmatched profit growth even when other global biggest banks are exiting the market. Unlike, the exit by Standard Chartered, Lloyds Banking Group, and Royal Bank, HSBC is evolving as oil revenues decline to embrace the profitable corporate and investment banking where it leads the large state-owned banks. The decision to sell off its assets in the retail segments gives HSBC a commanding presence in Middle East region to tap into growth driven by non-oil sectors.

HSBC Performance in the Middle East

HSBC realignments of its operations in the Middle East reflects a forward-thinking strategy to benefit from exiting foreign banks. The bank is divesting in businesses it faces fierce competition from government-owned banks to boost profitability in divisions it commands market leadership. The approach saw the bank sell off its Lebanese business to Blom Bank (Reuters, 2016). It matched the decision to acquire Lloyd's personal and commercial banking division in UAE then with 8,800 customers and a loan book of $537M (McGinley, 2013). The competitive banking environment in the Middle East is compelling rearrangements the bank considers critical to boost its capital ratios. Such reveals in the merger with Oman International Bank in 2012, disposal of Jordan operations and termination of wealth management operations in Lebanon and Bahrain (Trenwith, 2015).

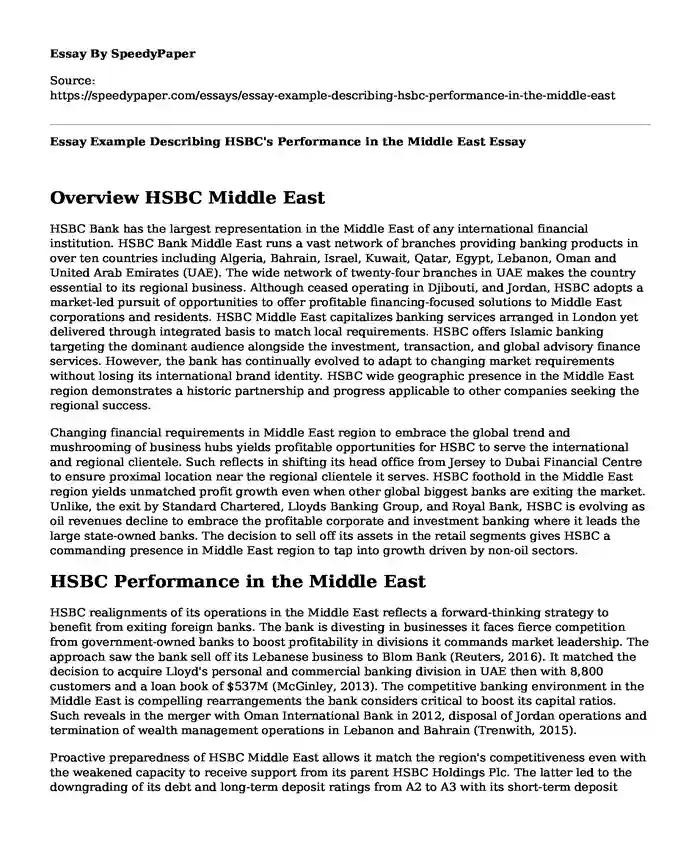

Proactive preparedness of HSBC Middle East allows it match the region's competitiveness even with the weakened capacity to receive support from its parent HSBC Holdings Plc. The latter led to the downgrading of its debt and long-term deposit ratings from A2 to A3 with its short-term deposit moved from Prime 1 to Prime 2. Its baseline credit assessment suffered a similar fate from A2 to A3 and affirmed at BAA2 (Kassem, 2017). The downgrade indicates the deteriorating operating environment in the strategic markets. However, HSBC Bank Middle East realignment efforts to tap into profitable niches saw its deposit ration moved from negative to stable. That demonstrates the expectation of its financial fundamentals retaining their current levels possible for its focus strategy to expand in the supportive operating environment. Its progress in the region reflects in the income statements indicating an improving trend despite the stiff competition as captured in Figure 1 below.

HSBC Income Statement Extract 2015 to 2017

2017

(US$000) 2016

(US$000) 2015

(US$000)

Net interest income 906,492 916,834 1,033,132

Net Fee Income 435,045 473,877 537,667

Net trading income 216,248 251,836 276,863

Net income from Financial Instruments 4,988 (209) 7,255

Dividend Income 3,872 2,609 8,230

Other Operating Income 126,320 29,079 (61,501)

Net Operating income 1,538,038 1,527,694 1,517,755

Profit for the Year 545,353 537,101 353,934

Figure 1 displaying HSBC Middle East income trend for three years, 2015 to 2017. Although experiencing declining net interest and fee income, the bank its operating income is growing steadily to maintain the positive growth in annual profit as displayed above.

HSBC Middle East Business Model

HSBC Middle East embraces a cost-cutting approach to trim its branch network in major markets by selling off in non-core operations and instead seeking narrowed and profitable model. Its strategy shows freeing from the competitive platform where online banks are wrestling off a significant market share. The bank approach involves a reorientation of the business by integrating technology into the core operations. The exit in Lebanon and Jordan indicates focused differentiation strategy to pursue core products. Doing so involves relieving the bank operations from non-core assets (Altman & Abughosh, 2016). Today's approach by HSBC features an internet banking platform blend with host-to-host delivery channels. HSBC integrated client management model favors the narrowed consultative approach in its core operations.

The consultative approach by HSBC Middle East targets real-time cash management to enable clients to optimize their financial operations using the host-to-host delivery channels. It targets assembling local and regional specialists to offer cash management solutions integrated seamlessly with business system services. The launch of this approach in the Middle East stimulated increased profitability in Middle East where UAE vast network leads other markets as shown in Figure 2 below. Although declining profitability in commercial, global banking, and markets, HSBC integrative approach targeting retail, wealth management, and corporate center is fruitful as displayed in Figure 2.

2017 Middle East Segment Analysis

Retail and WealthManagement Commercial Banking Global Banking & Markets Corporate Centre Total

UAE 110,156 52,702 256,909 45,468 465,235

Qatar 12,743 24,178 68,020 3,380 108,321

Rest of Middle East 10,911 24,435 10,667 17,788 63,801

Total 133,810 101,315 335,596 66,636 637,357

2016 Middle East Segment Analysis

Retail and WealthManagement Commercial Banking Global Banking & Markets Corporate Centre Total

UAE 83,349 93,608 284,554 7,242 468,753

Qatar 9,888 41,823 56,820 -4,705 103,826

Rest of Middle East 8,157 47,708 6,793 14,558 77,216

Total 101,394 183,139 348,167 17,095 649,795

The segment analysis above affirms the importance of the United Arab Emirates to HSBC revenue growth unlike other markets in the Middle East. HSBC Middle East management realizes this compelling it to prioritize UAE among Egypt and Saudi Arabia category. Citing regulatory setbacks, HSBC regards UAE open-door policy important to satisfy its growth strategy. Its exit from low-performing markets to expand operations in UAE and Saudi Arabia affirms its commitment to delivering increased value to its shareholders through the pursuit of the future growth opportunities in the government-led efforts to open their economies. Its overhaul strategy saw the bank refine its market strategy to shed off loss-making units and instead reshape its portfolio to match the fast-growth requirements in the region. Such reveals in the 2017 revenue growth in UAE as displayed in Figure 3 below.

HSBC uses a differentiated market penetration strategy tailored to suit the operating environment features. Its operation in UAE features alignment to the Dubai International Finance Center given the less regulatory requirements for international banks. This places its operations under the Dubai Financial Services Authority unlike in other Middle East markets where it operates under the country's central bank. The relocation allows HSBC align its operations within the region to a location dictating the regions business climate. The decision indicates the commitment to reinforce its attractiveness and competitiveness in the United Arab Emirates and international players with interests in the region. Beyond the national economy focus, moving to DIFC places HSBC Middle East at the center of financial communities attracted to a region soon becoming a global financial hub.

Competitor Comparison

Recent approach by Lloyds Banking Group features a divestment strategy by selling its international private banking. The decision to embrace simplifies business strategy emerges from pressure to terminate its loss-making entities in the competitive banking market. The decision to close and focus on lending in the UK's domestic market affirms Lloyds Banking Group struggles to profit from the transforming Middle East market. Llyods poor performance emerges from the mismatch in its products despite an established footprint comprising 8,800 customers in its personal and commercial segments (Kerr, 2012). The struggles led to selling its private banking to Union Bancaire Privee. The sale resembles the acquisition of its onshore assets and liabilities in the United Arab Emirates (McGinley, 20113). Lloyds Banking Group should embrace HSBC approach to transform its onshore business operations. Like HSBC the company failure shows need to exit the non-core operations to seek growth of its core operations.

Financial institutions exiting the Middle East markets including Lloyds and Barclays should consider adopting the HSBC's differentiated market penetration strategy to align its operations with the market requirements. Although HSBC sold off operations in the low-growth markets that enabled it to pursue high-growth in UAE, Egypt and Saudi Arabia (Zhou, 2018). Shedding off the loss-making units allowed it reshape the portfolio to match the fast-growth requirements in the region. Citing regulatory setbacks, HSBC regards UAE open-door policy important to satisfy its growth strategy. HSBC supports the growth strategy using a cost-cutting approach implemented across its branch network (Barbuscia, Roy, & Azhar, 2018). Doing so will enable the companies to accomplish a competitive edge to win a sizeable market share in their core operations. In addition, creating an integrated client management model will enable the banks to offer services using the host-to-host delivery platform.

HSBC success in applying the consultative approach allows it profit from real-time cash management requirements in the Middle East. Fellow struggling lenders could embrace a similar strategy by assembling their global expertise that should partner with regional and local specialists to create banking products that address the needs of Middle East. The decision by HSBC to adopt a glocal strategy allows it overcome the pitfalls international banks have experienced when they stick to their global products. Such creates possible conflict and mismatch of their products and market requirements, thereby compelling their exit. Consequently, the banks should learn from HSBC approach integrative approach to offer products and services of global standards adjusted to suit the local requirements.

Cite this page

Essay Example Describing HSBC's Performance in the Middle East. (2022, May 20). Retrieved from https://speedypaper.net/essays/essay-example-describing-hsbc-performance-in-the-middle-east

Request Removal

If you are the original author of this essay and no longer wish to have it published on the SpeedyPaper website, please click below to request its removal:

- Free Essay on Immigration Reform Bill

- Free Essay with the Case Study of International Organization Media Company

- Sports Marketing Essay Example: Marketing Strategy for A Park and Recreational Agency

- Essay Sample on Improving Leadership in Teams

- Essay Sample: Compassion in Undermining Political Suffering and Politically Achieved Rights

- "How to Say No" Speech - Paper Example

- Free Essay on the Tragedy of Antigone

Popular categories