| Type of paper: | Essay |

| Categories: | Data analysis |

| Pages: | 5 |

| Wordcount: | 1104 words |

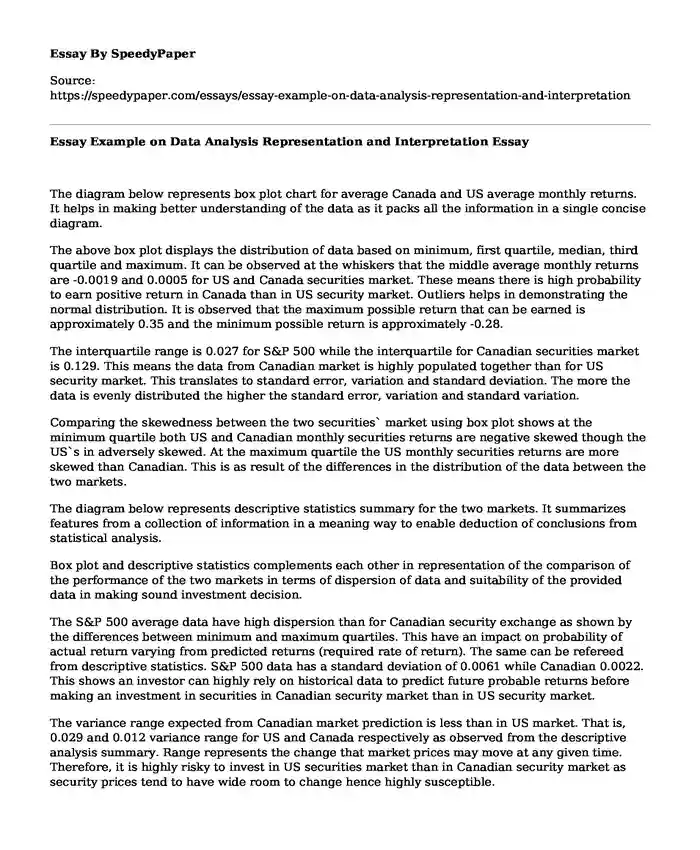

The diagram below represents box plot chart for average Canada and US average monthly returns. It helps in making better understanding of the data as it packs all the information in a single concise diagram.

The above box plot displays the distribution of data based on minimum, first quartile, median, third quartile and maximum. It can be observed at the whiskers that the middle average monthly returns are -0.0019 and 0.0005 for US and Canada securities market. These means there is high probability to earn positive return in Canada than in US security market. Outliers helps in demonstrating the normal distribution. It is observed that the maximum possible return that can be earned is approximately 0.35 and the minimum possible return is approximately -0.28.

The interquartile range is 0.027 for S&P 500 while the interquartile for Canadian securities market is 0.129. This means the data from Canadian market is highly populated together than for US security market. This translates to standard error, variation and standard deviation. The more the data is evenly distributed the higher the standard error, variation and standard variation.

Comparing the skewedness between the two securities` market using box plot shows at the minimum quartile both US and Canadian monthly securities returns are negative skewed though the US`s in adversely skewed. At the maximum quartile the US monthly securities returns are more skewed than Canadian. This is as result of the differences in the distribution of the data between the two markets.

The diagram below represents descriptive statistics summary for the two markets. It summarizes features from a collection of information in a meaning way to enable deduction of conclusions from statistical analysis.

Box plot and descriptive statistics complements each other in representation of the comparison of the performance of the two markets in terms of dispersion of data and suitability of the provided data in making sound investment decision.

The S&P 500 average data have high dispersion than for Canadian security exchange as shown by the differences between minimum and maximum quartiles. This have an impact on probability of actual return varying from predicted returns (required rate of return). The same can be refereed from descriptive statistics. S&P 500 data has a standard deviation of 0.0061 while Canadian 0.0022. This shows an investor can highly rely on historical data to predict future probable returns before making an investment in securities in Canadian security market than in US security market.

The variance range expected from Canadian market prediction is less than in US market. That is, 0.029 and 0.012 variance range for US and Canada respectively as observed from the descriptive analysis summary. Range represents the change that market prices may move at any given time. Therefore, it is highly risky to invest in US securities market than in Canadian security market as security prices tend to have wide room to change hence highly susceptible.

The resultant median in both box plot and descriptive statistics summary shows that the Canadian market for the period analyzed is positive (+0.0003 or 0.005) while for S&P 500 is negative (-0.0003 or -0.002). It shows that the majority of US securities return have negative returns as per the sample months analyzed while in Canadian securities market majority of the securities returns earned positive return. It can be inferred that it is highly risky to invest in US securities market than Canadian securities market.

In comparison of the standard errors at 95% confidence level, it can be deduced that Canadian securities information is highly reliable for decision making than US security market information. The standard errors are 0.004 and 0.00117 for Canada and US security markets respectively. The confidence levels are 0.00087 and 0.0024 for Canada and US security markets respectively. The higher the standard error the low the reliability of the data in making sound decision. The standard error may be reduced by increasing the sample size.

In consideration of suitability of the samples in being representative of the markets, Canadian securities market sample variance is less than for US security markets. The higher the sample variance the more susceptible the data analysis information in making sound financial decision like investment or securities sell out. It is highly probable the actual investment returns to be equal to predicted return in Canada than in US securities market.

The comparison of the two markets in terms of kurtosis and skewedness as observed from descriptive analysis summary. The results of the two statistical tools highly depends on the sample size. Skewness helps to assess the extent to which the average monthly securities returns are distributed in the two markets. Kurtosis helps to measure the amount of probability between the two tails or peakedness of a distribution. The Canadian security market data is highly skewed to the left tail (-1.9314) than US market (-0.473). Hence, future returns might reduce and the data is not normally distributed. The comparison in terms of Kurtosis, US market has 1.273 while Canadian market has 6.164, this reflects that the distribution of Canadian market is too flat. The Canadian data has lighter tails than normal distribution as it has Kurtosis higher than 3. The distribution is simply leptokurtic.

The diagram below represents monthly returns time series of the performance of Canadian and US securities market. It helps in visual representation of the relationship in the monthly average returns between the two markets.

The months that had highest variances in returns between the two where Canadian securities market had out performed US securities market in terms of returns are October and November 2018 and March 2020. US securities market had earned better returns than Canadian on December 2018, January and October 2019. The average securities returns are almost equal in the two markets on May 2018, and April 2019.

The Canadian securities market has average relative stable variance from one month to the other than US securities market as observed on the graph. This shows that Canadian market is less risky hence recommended to long-term and risk averse investors. The US security market is suitable to risk takers as the market price changes are highly susceptible to change. The US security market is highly risky but suitable to short-term investors as the returns are high.

The two markets curves move in the same direction. The only difference is in rate of market return changes where it is high in US securities market.

Conclusion

In conclusion, the Canadian market is suitable to low profile risk takers investors as investment required rate of return does not vary a lot from actual returns. The US securities market is suitable for speculators as actual returns on investment may vary significantly from the predicted returns. According to efficient-market hypothesis, Canadian securities market is highly efficient than US security market.

Cite this page

Essay Example on Data Analysis Representation and Interpretation. (2023, May 31). Retrieved from https://speedypaper.net/essays/essay-example-on-data-analysis-representation-and-interpretation

Request Removal

If you are the original author of this essay and no longer wish to have it published on the SpeedyPaper website, please click below to request its removal:

- Free Essay Example: Electromagnetic Radiation, Visible Light and Human Health

- Biology Essay Example: Respiration and Photosynthesis Cycle

- Social Situation or Setting, Free Essay Sample for Students

- Essay Exampe: Deleuzes Concept of Desire

- Space Travel Essay Sample

- Free Essay Sample on Hydrogen Cyanide Handling and Safety Measures

- Essay Sample on Communism: A Classless System With Communal Power for Improved Poverty Alleviation

Popular categories